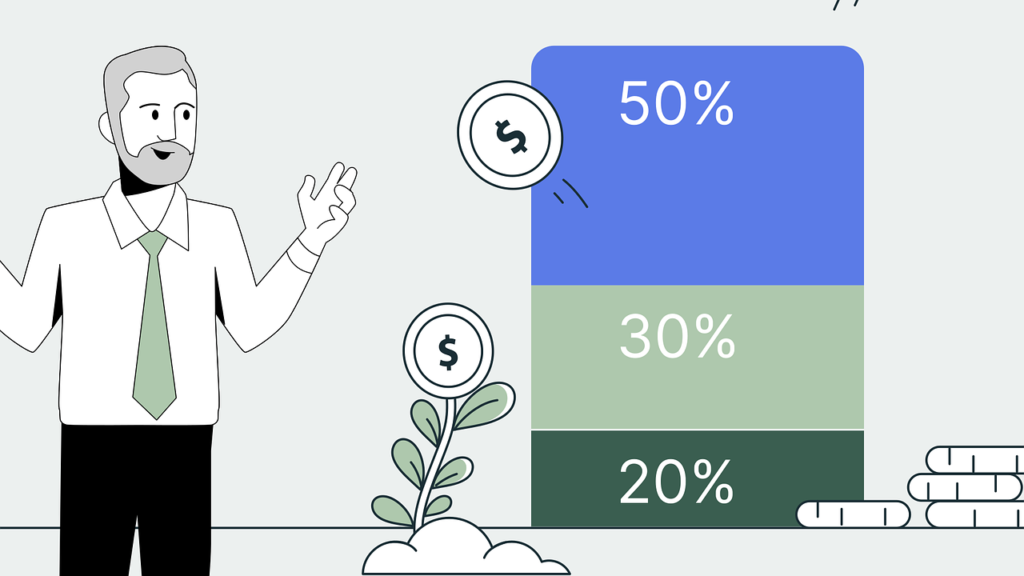

The 50 30 20 budget is a simple yet powerful framework for managing your money. It divides your after-tax income into three main categories: 50 percent for needs, 30 percent for wants, and 20 percent for savings or debt repayment. This approach provides structure without being overly complicated, making it accessible to anyone, regardless of income level or financial experience. Many people struggle to balance spending, saving, and debt management, but the 50 30 20 method offers a clear roadmap to achieve both short and long term financial goals.

This budgeting framework begins with identifying your needs. These are essential expenses required to maintain basic living standards, such as rent or mortgage, utilities, groceries, transportation, and insurance. Allocating half of your income to needs ensures that your essentials are covered while leaving room for flexibility in other areas. The next category, wants, includes discretionary spending like dining out, entertainment, hobbies, or non essential shopping. Limiting wants to 30 percent helps you enjoy life without overspending or compromising financial stability. The final 20 percent goes toward savings or paying down debt. This portion builds financial security, funds future goals, and reduces financial stress.

One of the key benefits of the 50 30 20 budget is its simplicity. It does not require tracking every dollar or creating complex spreadsheets. Instead, it provides broad percentages that guide spending and saving decisions. This framework also encourages discipline while maintaining flexibility. You can adjust the percentages slightly based on your personal circumstances, such as increasing savings or accommodating higher fixed expenses. By following this structure, you gain clarity, control, and a balanced approach to financial management.

Implementing the 50 30 20 budget begins with calculating your after-tax income. Start by listing your monthly essential expenses. For example, if your rent is eight hundred dollars, utilities are one hundred fifty dollars, and groceries are three hundred dollars, these costs are part of the 50 percent allocated for needs. Next, review discretionary spending for the month. Dining out, subscriptions, and entertainment fall under the 30 percent category. Assigning specific amounts to these items helps maintain control without feeling restricted.

The final 20 percent goes toward building savings or paying off debt. This could include contributions to an emergency fund, retirement accounts, or extra payments on credit cards or loans. For instance, if your monthly income is three thousand dollars, six hundred dollars would go toward savings or debt repayment. This consistent allocation helps grow financial security over time and prepares you for future goals.

Automation can make the 50 30 20 approach easier to follow. Setting up automatic transfers to savings accounts or scheduling payments toward debt ensures consistency. It reduces the temptation to spend money intended for savings and builds a routine that reinforces financial discipline. Monitoring spending periodically allows you to adjust as needed, ensuring the budget remains realistic and aligned with your lifestyle.

Flexibility is also important. Life is unpredictable, and unexpected expenses can arise. Adjusting the percentages temporarily while maintaining focus on the overall structure allows the budget to remain effective without causing stress. For example, a month with higher medical costs might require reducing discretionary spending or slightly lowering savings, while maintaining the long term goals.

The 50 30 20 budget also encourages financial awareness. By regularly reviewing spending in each category, you understand where your money goes and identify opportunities for optimization. Over time, this awareness builds stronger money habits, reduces unnecessary expenses, and supports consistent saving.

Following the 50 30 20 framework helps balance spending, saving, and debt management in a manageable way. It provides structure without being restrictive and promotes intentional financial decisions. By committing to this approach, you can improve financial stability, achieve goals, and reduce stress associated with money.

This budgeting method is a practical tool for long term success. It provides guidance, encourages discipline, and builds a foundation for financial growth. The 50 30 20 budget allows for flexibility while promoting responsibility, helping you make progress toward short term needs and long term aspirations. Consistent application creates confidence and control over your financial future.

For more one budgeting, have a look at our article Practical Budgeting Tips for Everyday Life.